Keeping

Good Records is fundamental to efficient

operation of a telephone

company, both for efficient management of resources and for smooth

dealings

with customers, regulators and others, - - - suppliers, for

instance.

Where record keeping suffers, it often is because the company outgrew

the

system, which may have been designed when the company was tiny and

clearly

didn't need a lot of "unnecessary paperwork".

....Office

routines differ greatly in different sized companies. but they all

share

the same common goals: to supply all customers with high quality

service

at the lowest cost; and to provide the company investors with the

highest

return possible on their investment, consistent with the first goal.

....Each

of these two goals includes several components. Thus, the goal of

providing

high quality services means: 1) establishing the service promised; 2)

keeping

circuits clear, strong and trouble free; 3) restoring interrupted

service

as quickly as possible; and 4) providing accurate billing (not within

the

scope of this text.)

....Similarly,

giving company investors the highest possible return depends on: 1)

being

able to connect or restore service quickly, without error; 2) making it

possible to use fully each unit of plant in place; 3) using orderly

company

procedures to help employees do their best; 4) supplying engineering

personnel

with accurate information on maintenance problems, plant traffic, fill

and actual costs; and 5) keeping on hand only the required stock.

....The

trend that ties these components together is record keeping. Because

records

are vital to the efficient operation of the company - - - whether

it is plant, engineering or customer records, it is important that all

personnel, craft and administrative, have a good understanding of the

needed

forms and records in order to help them do their jobs better and keep

the

basic system up to date. Not only will such an understanding give telco

personnel ideas on how to improve their own routines, it will help them

contribute to achieving the basic company goals.

Purchasing

....Purchasing

is the process of ordering, paying for and stocking an item of

material.

It is the first action taken after a careful decision has been made to

add a section or item of telephone plant, or to add to the stock of

in-site

supplies.

....Telephone

plant can be purchased in two ways, through a contractor or by

purchasing

material through a supplier and placing it with your own crews. When

plant

is purchased by contract, the contractor's invoice includes an itemized

list of each unit's cost. the units are debited to a Construction in

Progress

account where you may have to add some of your own costs or your

engineer's

costs to the unit's cost. In ordering your own plant, the quantity,

type,

size, and cost for large plant additions should be made to you by the

engineer.

....Controlling

the costs of purchases is a must these days. Consider three ways to do

this: 1) Call each supplier and obtain the current prices. 2) Have the

supplier keep you posted on current prices. 3) Use your experience on

which

supplier has the lowest price on each item.

....The

inventory record form also should be arranged so the quantity in stock

and the timing of order placement can be controlled, thereby making it

possible to budget costs through the year.

....In

the past, the person responsible for making purchases may have handed a

list to a supplier making a routine call. Or the purchaser may have

telephoned

the supplier to give the order. These actions should be practiced only

in emergencies. Instead, have printed your own company pre numbered

ordering

form. Use it for all purchases made. See

Figure

1 Doing this, you will always know what you actually ordered,

when

you ordered and why you ordered. Finding what you ordered, when there

is

a question, will be simplified because you follow a set routine

in

making purchases.

....If

you are an REA borrower, have your assigned number set in the heading

of

your order form, with instructions on the back. This way, you will have

on each order, written notice to the supplier that the items shipped

must

be approved items.

....Remember

to have your inventory record in front of you when making out an order.

Always check it to make sure that you have not missed an item.

....All

orders must be approved by the manager or by an assigned agent. Copies

should be distributed within the company to three points. One

is

the person responsible for receiving the material. This person will

know

exactly what is being ordered, have an idea when it will arrive and to

whom it is to be delivered. A second copy should go to

"accounts

payable", so they will know who has ordered material, what item is

expected

and what cash should be available to pay for the purchase. A third

copy should go to persons responsible for completing a project, so it

is

known that the project is being followed through, as

planned.

....If

material must be ordered by telephone, have a purchase order number

ready,

telephone the order and give the supplier the order number. Then send a

copy of the order to the supplier, confirming the call, and handle the

order within your company as a normal order. This will keep the routine

normal, both at your company as well as at the supplier's offices.

....Some

companies, especially those with district offices, must have a form

which

precedes the making of a purchase order. This is called a Material

Requisition. See

Figure 2 Small companies may type a purchase order from a list

written on a scratch pad; however, the larger company's purchasing

department

must know permission has been given before the typing of a purchase

order

is done. The requisition form therefore is necessary. Telephone

orders

must be confirmed in requisitions also. You may even have to call long

distance to your purchasing department to obtain an order number. Keep

the routine normal.

When

the Order Arrives

....Receiving

material is the process of opening freight or parcels, checking the

enclosed

packing slip against the actual contents and filling out the Record of

Receiving form See Figure 3. This

form

sets up a consistent routine on keeping a good record of material.

Also,

this form makes it possible to eliminate indicating which account or

accounts

a check is made out for, only the receiving number need be recorded on

the supplier's paycheck. Of course, only one supplier's material can be

recorded on any one Record of Receiving.

....Having

the person who receives the material, fill in the stock numbers is more

reasonable because that person usually is more knowledgeable about the

material. The spaces marked "A" on the sample in Figure 3 will

be

filled in by the receiver. The packing slip then is kept in the

receiving

files, or it can be sent as a notice of receiving to persons

responsible

for a specific project.

....Accounting

personnel, filling in the spaces marked "B", will use the form

further

to price out the units, pay for them and then transfer the costs to the

proper accounts.

....Paying

for units of a contract also can be achieved on the Record of Receiving

from. The contract units then are transferred to a Construction in

Progress

account.

....When

receiving and checking a shipment reveals an item that cannot be used

because

it is damaged or it is the wrong item, place a "D" for damaged or a "W"

for wrong in the Condition column. Then set the item aside and make

arrangements

to have it returned. The Notice of Goods Returned or Transferred form

then

is filled out See Figure 4. The

company

still will receive an invoice for all the items shipped and pay it in

full.

A credit will be issued by the supplier for goods returned. The

Accounting

department keeps the goods returned form on file, which is a record of

cash paid out, even though it is not put into inventory. Checking this

file periodically can reveal any credit not honored, and then proper

steps

can be taken to see that credit is issued. This form also is filled in

by the person sending the goods spaces marked "A" and accounting

marked "B".

Inventory

....Inventory,

to company supervisors and executives, means to have materials or a

record

of materials in stock, ready for labor employees to place in plant.

Inventory,

to a labor employee, can mean that he or she will count and list all of

the material in stock on a given day each year. Both of these

definitions

are correct; however, a more meaningful one is that inventory is money

invested, which the company cannot earn a return on.

....It

takes a pretty good plan to keep the inventory down and have material

in

stock when it is needed. You have to know when you can buy at a larger

quantity in order to cut purchase cost. There must not be excess

material

that will sit around for years. Also, if money is not spent, it is

available

for other needs or is in the bank earning interest. Nowadays, there are

suppliers who give good prices on small quantities and can give 24 hour

delivery. Shop around.

....There

can be three methods used to keep a record of your stock. One

is

to keep count and cost of each separate item you buy until it is

actually

working in plant. The second is keep count and cost only of the

items which are identifiable as installable units, then combine the

costs

of the small items, such as screws, tape, etc., into an Exempt Material

account. The exempt material costs are spread by percent of average

use,

over several accounts. The costs do not need to be on record as being

in

stock. The third method is not to put the material cost on

inventory

but charge it directly to a Work Order in Progress account and store

the

item in a separate location until it is in plant. This is not a good

practice

because some person may pick up an item and put it in plant somewhere

else

by mistake, or even if he knows he should not do it. Use this third

method

only with vehicles tools, etc.

....The

first inventory method should be used at warehouses where the small

items

move quickly as large items, and the inventory must be on hand to

distribute

to branch or district stockrooms. However, it may be necessary to

inventory

all items if there has been a history of theft or overstocking, using

this

method only until the problem has been corrected. The large stockroom

may

do all items also, but costs in bookkeeping still will not include

exempt

items. There are extra costs encountered by counting and reporting the

use of each screw and bolt: (1) it requires one third more time to fill

out a time report or cost out a work order; (2) it takes twice the time

to keep inventory throughout the year; (3) in a small company, all

stock

would have to be locked up, making it necessary to have one person

available

full time to distribute material.

....The

use of the exempt material method is recommended for all companies with

more than 2000 stations. The cost difference for smaller companies to

record

all items will not be significant, and they still may elect to use that

method, if law permits.

....Inventory

procedures must be set up so that transfer of costs and materials from

stock are easily understood and free from errors. The process starts

with

the receiving of material. After the material is received and placed on

the inventory record, it is ready to be distributed.

....As

previously mentioned, the cost record of the material will end up in a

ledger book, by account. To aid the process of transferring the costs,

it is best to assign stock numbers to each item on inventory. The

numbers

can be made up of five, six or seven digits, whichever works best. They

should be designed to be descriptive of the piece of material. The

engineer

then can use the number on the work order plans, which in turn tells

the

laborer what unit to place. The laborer then can place that same number

on his or her time sheet, without having to check which number to use.

....The

first two "digits" in the stock number should be letters that describe

the type of unit it is. The remaining digits describe size, in the

metric

system, where applicable, If the first two letters can be the same as

property

records, use them.

Examples:

CA10124

.......4

= 24 gauge

012 = 12

pair

........1

= AP sheath

CA =

cable..

|

ST10039

.......039

= 30 millimeter

.....10

= galvanized

.ST

= strand...

..

|

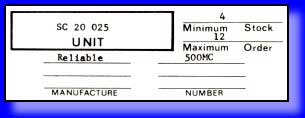

SC20025

025 = fits cable

up to..

...............25

millimeters in dia.

20 = for

plastic

fig. 8

SC =

splice closure..

|

|

|

....The

stock numbers must be placed on labels which are on the shelf under

each

item in the store room. The daily time sheet must be designed to accept

these numbers and so should service orders and work order closings.

....The

example shown in Figure 5 is for a splice closure. When the inventory

is

down to about four, order 12 more. The card should be made of a

material

which can be written on or changed.

.......................................................................

|

The label also should

be used for exempt material. In place of the stock number, place

a description of the material.

Example: Screws, Stainless steel,

round 3/4 x 8.

A careful study and

plan, made by the manager, plant superintendent and accounting is

needed to fill in the maximum and minimum quantities. Each year's

inventory will show if the plan is working well.

If your stock shelf's are too thin for this

label, the manufacturer's name and number can be moved up to the right,

or it could be removed. The reason for listing the manufacturer is to

eliminate having to look in the catalog.

Exempt

Material:

Material being invoiced which is

commonly used on many different items or parts of items but is costly

to inventory is partially charged to an Exempt Material Account and the

remainder is spread over Maintenance. As inventoried items are put to

use in plant through a work order or service order, Exempt Material is

also charged out. The ratio of total inventory in stock in relation to

total exempt material in stock, is applied to the inventory just placed

in plant. The result is the value to be credited from Exempt Material

and charged to Plant.

The ratio used

will not remain the same because of the continual purchases being made.

If more exempt material is purchased, more will be charged out.

The card used to keep record of each different

inventory item can be used to keep the balance of

|

|

exempt material. This card will be

described later in the series.

The invoice which contains one or more units

of exempt material could have the quantity spread figured out on the

back of the invoice. The payment check then could be charged to each of

the spread accounts. However, this takes many more entries to the

ledgers and also can take up too much space on the check stub.

When filling out the

receiving report (Figure 3),

note that at the right edge there is a column to place a Material

Holding account number. This account is used to combine several

invoices before spreading the costs to Exempt Material or Maintenance.

At the left of the account numbers is a column to place a code which is

used to tell how a cost is to spread from the Material Holding account.

|

Figure 6

|

|

Figure

6 lists some units with code letters. A sheet used to spread the

material in holding, according to the code, is shown in Figure 7. The

total cost, listed just left of the code number on the receiving

report, is placed on the spread sheet under the corresponding code.

Receiving report costs, with several units of the same code, are added

together, with that total being placed on that spread sheet.

A routine time is picked to credit this holding account

and debit

the Maintenance or Exempt Material accounts. On your spread sheet,

total each coded column and spread that total according to the

percentages noted within the boxes below, placing the broken down costs

in

|

the boxes. Each horizontal line then is

totaled to the left, giving

you the total cost to debit the noted account.

The

percentages used to spread each column are the results of a careful

study made by your personnel as to where each piece of material might

be used in maintenance. For example, vinyl tape is placed in column

"U", 20% is used Exempt Material, 20% is used for the repair of aerial

cable, 20% for buried cable, 10% for central office or carrier and 30%

for station connections. Is this right? You had better find and back

your own figures, or use the REA recommendations.

Go To Book

Index

|